Creating a perfect seed round with Leads, Follows, Angels and Random investors

For a startup, raising a seed round is a daunting endeavor. Techstars Seattle Demo Day is looming, and I recently finished mentoring the teams at the Kaplan EdTech Accelerator. I’ve written about fundraising before here and here, but I recently saw Brad Feld (who is awesome and was an investor in my last company) give a great talk that added a few great words to the lexicon – Leads, Followers, and Random investors. So, borrowing from Brad and adding my own ideas, here are a few things to consider when putting together that perfect seed (or any) round.

First, some definitions;

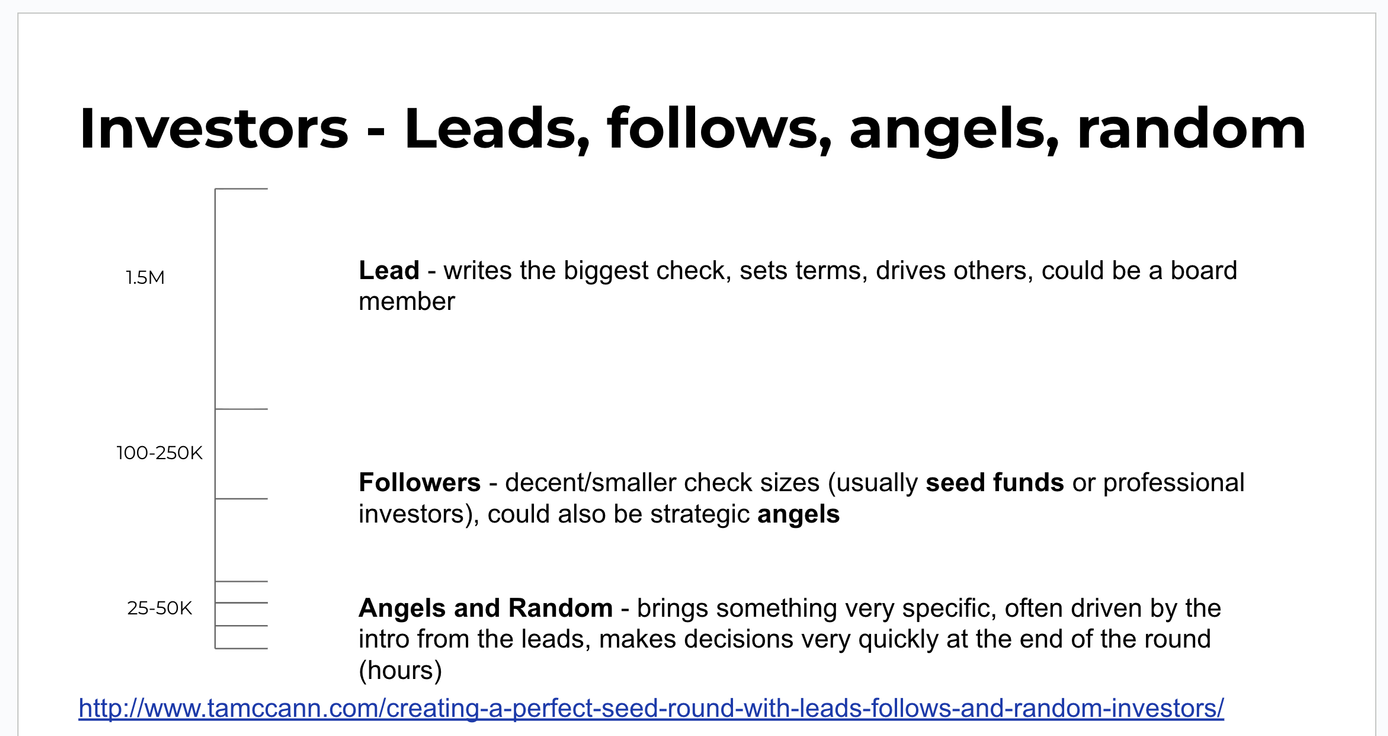

Leads – Usually professional investors and VCs, who write > 5 checks/year at $500K-5M/deal to fund startups. They are experienced in the dance, the terms, and know lots of other investors… and understand how it all works. They negotiate with the entrepreneur and help set the terms for a round. These people will usually take a board seat too, so you should pay special attention to how they engage you, make decisions...

Followers – These are usually smaller funds, family offices, accelerators, or professional angels. These are the majority of the investors you will meet. They either don’t have the time, money, expertise, or fortitude to lead (price, negotiate...) a round. But, they can be very valuable to add expertise, connections, and be a channel to the lead investors. Followers usually write checks from 100-1M/deal.

Angels - These people might have a day job and invest as a hobby, to engage with startups, or to support the startup community. If they are “active,” they usually do at least 4-5 deals/year. I am an angel and very clear about it with companies, but many other investors are not. Angels tend to write checks from 10-100K/deal.

Random - will be the ones that one or more of the other types introduce to you, once they've committed. You will likely not know them going into the fundraising process and might not even know them afterwards. Still, they can add lots of "name brand" value and legitimacy to your company and really fill out a round "narrative.

The overall fundraising process should be planned (e.g. I hope to close by the end of the year), with a solid understanding of how much you want to raise (e.g 2-3M), with what vehicle (e.g. convertible note or priced round), and under what terms (e.g. 8M cap, 18-month term, 20% discount). Much more on terms here and in Brad’s book Venture Deals. The clearer you are, the faster the round will likely come together.

With this plan, you have a sense of the amount you need from a Lead investor, usually >25-50% of the total raise. You also have a starting point for negotiation when you get the lead investor in the room. Now your job is to go find the LEAD!

In the best case, you will also have some idea of the domain expertise (e.g., “marketing tools”) and/or functional experience (e.g., content marketing, channel sales, product development…) of your desired investors, and you can ultimately create a “tapestry” of people with complementary skills and backgrounds to add to your company.

When you start talking to investors, spend time asking questions to determine a good fit. Ask them directly;

- How much do you typically invest /company?

- How many deals/year?

- What thematic areas are you most interested in?

- When you invest, how do you like to engage with the company?

- When you have invested in the past, were you a lead or a follower?

- In addition to the money, how else do you like to help your companies?

An experienced investor (the kind you want) will be totally comfortable with these kinds of questions. They, too, are about expediency: getting to a YES or NO as quickly as possible and not wasting their or your time. Depending on their answers, you will get a pretty good sense of the kind of investor they are and, in the best case, how likely they are to invest in your space and whether you think they can really help the company.

Assuming you think there is a good fit, continue the discussion about the business, the opportunity, and the specifics to get to a “yes, I think I would like to invest.” If they are a Lead, you can start working toward a term sheet; if they are a Follow, “collect” them for later and communicate this to them, something to the effect of “Hey T.A., I am really excited to work with you, and I think you could add real value to our company. Right now, I am focused on finding our lead investor to get to solid terms, but I would love to pencil you in for (X, depending on their answer to normal check size) for the round. How does that sound?” At this point, consider them “soft-circled” and get back to finding the lead.

Followers are not likely to become leaders, no matter how much you try to convince them. Too many entrepreneurs spend way too much time trying to make this conversion happen. If someone who has not led before wants to step up, probe on experience, skills, desire… and plan to invest more time with them and your lawyers to get to a solid term sheet, but this is not the desired path. You really want an experienced Lead.

After many meetings, you are likely to end up with a collection of Followers and finally, a LEAD! Woot! Get to a term sheet, get the Lead committed, and then start closing the Followers. Depending on where in the process you found the Lead, you may have a long or short list of potential Followers. Part of the job of the lead, is to bring more people to the table. Ask for introductions and leverage their leadership to close others. Assuming the lead has 25-50% of the round, Followers might close out the round or at least get to 75% before you need to go back to the well and look for new investors.

Follow the same process with the Angels. As you build the domain, functional, and market expertise, you might choose different angles. You might need to force them into smaller check sizes, and it might (or should) get competitive to get into the round.

But wait, there’s more. As you diligently move through your known prospects, getting people to commit, “random” people will show up and express interest. These are likely people who have heard about you from another investor, another entrepreneur, or a press article… but they feel random. As these investors are coming late in the round, you should have momentum with lots of others signed up, closing these Random investors much more quickly. Otherwise, rinse and repeat the process above, but be OK with Random happening.

Finally, fundraising is a sales process, so you need to keep the momentum going with lots of prospects, closing when you can, and continuing the conversation with others, being clear, consistent, and regular with your communications.

And, if you need a template to run your process or keep a list of your potential investors, check this out.